What Readers Need to Know

- Pension drawdown allows DC pension savers to take flexible income from their pension pot.

- Up to 25% can normally be taken tax-free, subject to the Lump Sum Allowance.

- Taxable Income from drawdown is taxed at the saver's marginal rate.

- Flexibly accessing a pension can trigger the MPAA — reducing future DC contribution capacity.

- Free guidance is available via Pension Wise; personalised advice from a regulated adviser is recommended.

Introduction

Pension drawdown has become the dominant way UK retirees take income from defined contribution pensions since pension freedoms in April 2015. For many savers, it offers the right balance of flexibility, tax efficiency and ongoing Investment exposure.

This article explains, in plain British English, what pension drawdown is in the 2026/27 tax year — the main Options, the tax outcomes and the risks to weigh. It is general information for UK readers and does not constitute personal advice.

Pension Drawdown in One Sentence

Pension drawdown is a way for UK savers with defined contribution pensions to take variable income from their pension pot while leaving the rest invested.

Where Drawdown Came From

Drawdown existed in limited form before 2015, with Government Actuary's Department (GAD) caps on the income that could be taken each year. Pension freedoms in April 2015 introduced flexi-access drawdown, removing the cap and giving savers freedom to choose how much income to take, when. The reforms also created the Money Purchase Annual Allowance (MPAA) to limit further DC contributions after flexible access.

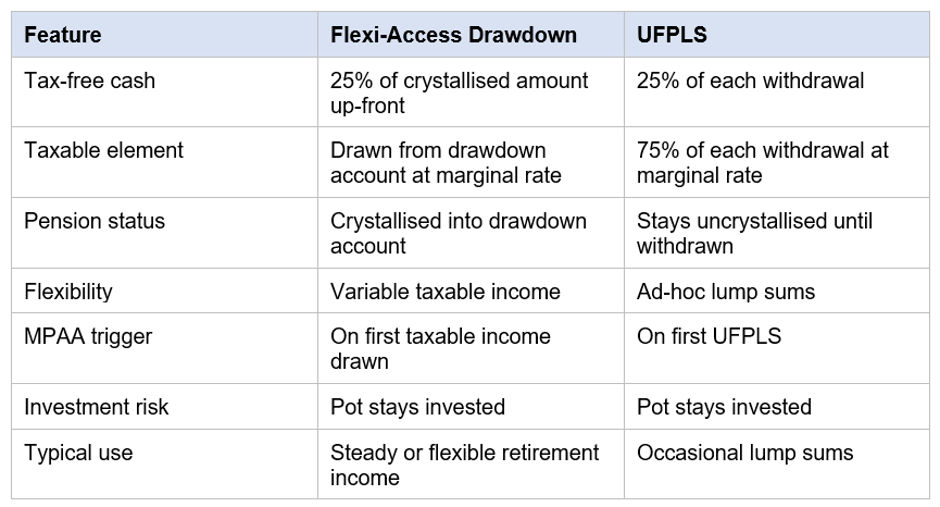

Flexi-Access Drawdown

Flexi-access drawdown is the main method. The saver crystallises part or all of the pension, takes up to 25% as a tax-free Pension Commencement Lump Sum (PCLS) and moves the rest into a drawdown account. The drawdown account stays invested and supports taxable income withdrawals at the saver's discretion.

UFPLS

Uncrystallised Funds Pension Lump Sums (UFPLS) are an alternative. Each UFPLS is 25% tax-free and 75% taxable. The pension stays uncrystallised — there is no separate drawdown account. UFPLS suits savers wanting ad-hoc lump sums rather than steady income.

Tax-Free Cash and the LSA

Up to 25% of the crystallised amount can normally be taken tax-free. The lifetime cap on tax-free cash is the Lump Sum Allowance (LSA) of £268,275, introduced from 6 April 2024 to replace the lifetime allowance. The Lump Sum and Death Benefit Allowance (LSDBA) of £1,073,100 sets the wider lifetime tax-free cap, including on death benefits before age 75. Existing fixed and individual protections may preserve higher limits for some savers.

How Drawdown Income Is Taxed

Withdrawals from drawdown or UFPLS that fall outside the 25% tax-free element are taxed as income at the saver's marginal rate. They sit alongside other taxable income — the state pension, employment, rental income — for personal allowance and tax band purposes.

The first taxable Withdrawal can suffer emergency tax under PAYE rules. HMRC normally refunds the excess automatically through the tax year or via a P55, P53Z or P50Z claim form.

The MPAA

Taking taxable income from flexi-access drawdown or any UFPLS triggers the Money Purchase Annual Allowance — £10,000 for 2026/27. The MPAA replaces the standard annual allowance for DC contributions. Carry forward of unused annual allowance does not apply to the MPAA. Taking only the 25% tax-free cash from flexi-access drawdown does not normally trigger the MPAA, but the rules are technical.

Drawdown and Annuities

Annuities exchange some or all of the pension for a guaranteed income for life or for a fixed term. Annuity rates vary with interest rates and the saver's circumstances. Many UK savers combine annuity purchase with drawdown — using the annuity to cover essential expenditure with a guaranteed income, and using drawdown for flexibility and growth.

Investment Risks in Drawdown

- Investment risk — values can fall as well as rise.

- Sequence-of-returns risk — withdrawals during market falls can permanently reduce sustainable income.

- Longevity risk — outliving the pension if withdrawals are too high.

- Inflation risk — fixed withdrawals lose real purchasing power over time.

- Behavioural risk — panic selling during downturns locks in losses.

Practical Drawdown Strategies

There is no single right approach. Common strategies include:

- Natural Yield — drawing only the income generated by investments to limit Capital depletion.

- Fixed percentage — withdrawing a set percentage each year, adjusting if portfolio value rises or falls.

- Guard-rail rules — adjusting withdrawals based on portfolio performance against targets.

- Cash buffer — holding one to three years of expected withdrawals in cash to ride out market falls.

- Bucket approach — dividing the pension between cash, bonds and Equity buckets for different time horizons.

Setting Up Drawdown in Practice

Drawdown is normally set up with the pension provider holding the DC pension. The saver completes a drawdown application, chooses whether to take tax-free cash up-front and, where required, selects a sustainable income strategy. Some workplace pensions do not offer drawdown in-scheme and require a transfer to another provider — often a SIPP — to use drawdown features.

Modern platforms support online drawdown set-up with downloadable tax statements. Older providers may require paper forms. Either way, the first taxable withdrawal can suffer emergency tax under PAYE, with HMRC Refunding the excess in due course.

Death Benefits and Beneficiaries

Pensions in drawdown can pass valuable death benefits to nominated beneficiaries. Death before age 75 normally allows benefits to pass free from UK income tax up to the LSDBA of £1,073,100. Death after 75 means beneficiaries pay income tax at their marginal rate on benefits received. The IHT treatment of pension death benefits is the subject of announced future changes; savers should follow current GOV.UK guidance.

Beneficiary nominations should be kept up to date and reviewed after major life events. Trustees use nominations as a key input when deciding to whom death benefits should be paid.

Combining Tax-Free Cash and Income

Many UK savers do not take all 25% of tax-free cash in one go. Partial crystallisations — where the saver crystallises some of the pension at a time, taking the 25% tax-free element of that portion — can spread the tax-free cash across several tax years. The Lump Sum Allowance continues to apply across all crystallisations, but the strategy can support a steadier income mix.

Another common pattern is to take all available tax-free cash up-front to pay off the Mortgage or fund a one-off purchase, leaving the rest in drawdown for taxable income later. Each approach has tax and cash-flow implications that benefit from professional input.

Where Drawdown Fits in UK Retirement Planning

Drawdown sits alongside the state pension, any defined benefit pensions, ISAs, GIAs and other resources. Many UK retirees integrate drawdown with the timing of the state pension and the use of ISA balances to manage tax bands. Drawdown can be combined with partial annuity purchase, ongoing employment income and inheritance planning. Professional advice is normally valuable.

Reviewing Drawdown Each Year

Drawdown is not a one-off decision. A useful discipline is an annual drawdown review covering current pot value, withdrawal rate against a sustainable target, cash buffer, asset allocation, beneficiary nominations and projected position five to ten years out. Many UK savers run the review with their adviser ahead of the new tax year, coordinating with other allowances and planning steps.

Where to Get Help

Pension Wise, through MoneyHelper, offers free appointments for over-50s with DC pensions, including SIPPs. The appointment is guidance, not advice — it explains options but does not recommend a specific product. For personalised recommendations, a regulated financial adviser should be engaged. The FCA Register lists authorised firms.

MoneyHelper also publishes general guidance on UK pensions and retirement income, including comparison tools, calculators and information on annuity rates and drawdown providers. Combined with regulated advice, free guidance can substantially reduce the risk of poorly informed retirement decisions. The FCA's ScamSmart resource is a useful starting point for spotting warning signs in any unsolicited pension offers, especially around the time of accessing benefits.

Drawdown Options at a Glance

The two main UK drawdown methods for 2026/27.

Key Takeaways

- Pension drawdown is the most common way UK retirees take income from DC pensions.

- Flexi-access drawdown and UFPLS are the two main methods.

- Up to 25% can be tax-free, subject to the LSA of £268,275.

- Taxable income is taxed at the saver's marginal rate.

- Taking taxable income triggers the £10,000 MPAA for future DC contributions.

- Investment, longevity, sequence and inflation risks all matter in retirement.

- Free guidance via Pension Wise and regulated advice both help.

Please wait processing your request...

Please wait processing your request...