What Readers Need to Know

- SIPP fees vary widely between providers and are typically a mix of platform charges, dealing costs and fund OCFs.

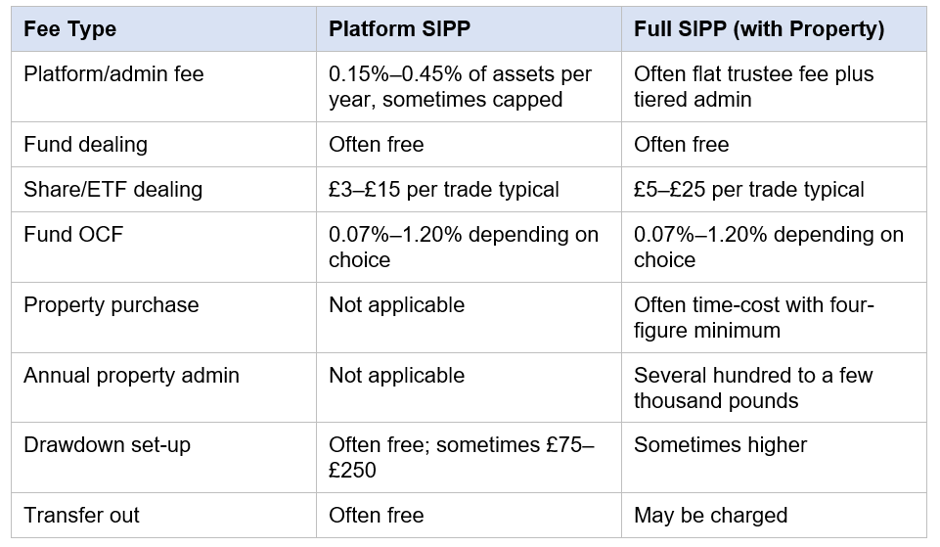

- Low-cost platform SIPPs may charge 0.15%–0.45% of Assets per year plus dealing fees; full SIPPs that hold property cost more.

- Fees compound over decades and even small differences materially affect long-term outcomes.

- Default funds in workplace pensions are subject to a 0.75% charge cap; SIPPs are not.

- Pension decisions involving charges, transfers and consolidation usually benefit from regulated advice.

Introduction

Fees are one of the most important and least understood elements of any UK pension. The Self-Invested Personal Pension (SIPP) offers savers a wider range of investments than a typical workplace scheme, but with more choice comes a more varied charging structure. Some SIPPs are very low cost. Others — particularly full SIPPs that hold commercial property — can be considerably more expensive.

This guide walks through the main categories of SIPP fees UK savers should expect to encounter in 2026/27 and the questions to ask before opening or transferring a pension. It is general information and does not constitute personal advice. Anyone considering opening a SIPP, transferring an existing pension or consolidating multiple pension pots should speak to a regulated financial adviser.

Why SIPP Fees Matter

Pension charges may look small on paper, but they compound over decades. A 0.5% difference in annual fees on a £100,000 pot over 25 years can be the difference between tens of thousands of pounds at retirement. UK regulators and the Pensions Policy Institute have long argued that charge transparency is critical for member outcomes.

Workplace pensions used for auto-enrolment are subject to a 0.75% charge cap on the default fund's fund management costs. SIPPs are not subject to this cap, which is one reason charges need careful comparison.

The Main Categories of SIPP Fees

SIPP costs typically fall into four broad categories. Each provider's published 'key features' document will set them out in full.

- Platform or administration fee: The ongoing charge for holding the SIPP wrapper, normally calculated as a percentage of assets, a flat monthly or annual amount, or a tiered combination.

- Dealing charges: Per-transaction fees for buying or selling shares, ETFs and Investment trusts. Fund trades are often free.

- Fund charges (OCFs): The ongoing cost of any investment funds held, deducted from fund returns. Common ranges run from 0.1% for passive trackers to over 1% for some active funds.

- Specialist or property fees: Full SIPPs that hold commercial property charge separately for purchase, ongoing administration, rent collection and sales.

Percentage vs Flat Fees

Flat fees

Some platforms charge a fixed monthly or annual amount regardless of pot size. This can favour larger pots, but a flat fee on a small pot can quickly outweigh any returns. Savers should compare on the basis of expected total cost, not the headline rate.

Dealing and Trading Costs

Dealing fees vary by asset type. Many platforms allow funds (unit trusts and OEICs) to be traded for free because they are dealt at end-of-day prices. Shares, ETFs and investment trusts traded on a live exchange normally attract a per-trade fee, plus 0.5% UK Stamp Duty Reserve Tax (SDRT) on most UK share purchases and the PTM levy on large trades.

Frequent trading can quickly erode returns. Long-term investors are usually advised to focus on a diversified, low-turnover portfolio rather than active trading inside a pension.

Fund OCFs and Underlying Costs

The Ongoing Charges Figure (OCF) of any fund held inside a SIPP applies on top of the platform fee. A low-cost index tracker may have an OCF of 0.07% to 0.20%. An actively managed fund may charge 0.50% to 1.20% or more. Investment trusts have their own structure with KIDs disclosing both ongoing charges and any performance fees.

Full SIPP Property Costs

SDLT is not exempt for pension purchases and is charged at the non-residential rates. VAT may or may not apply depending on whether the seller has 'opted to tax', and a Transfer of a Going Concern (TOGC) can change the treatment. Specialist legal and tax advice is essential before a SIPP buys property.

- Property purchase fees — often on a time-cost basis with a minimum charge that can run into four figures.

- Annual property administration — typically a fixed amount per year per property, covering rent collection, insurance reviews and compliance.

- Lease and tenancy work — drafting and reviewing lease documents, rent reviews and lease renewals.

- Sale, lender and re-Mortgage fees — applied when a property is sold or the SIPP refinances borrowing.

- Third-party costs — legal fees, surveyor fees, lender arrangement fees and SDLT.

Other Fees to Watch For

- Drawdown fees — some operators charge to set up or run flexi-access drawdown.

- Annuity purchase fees — for arranging the open market option.

- Exit and transfer-out fees — though the FCA has limited or banned these in many cases, savers should still check.

- In-specie transfer fees — for moving existing assets between providers without selling them.

- Foreign exchange charges — relevant for overseas shares and ETFs.

- Death benefit administration fees — applied when benefits are paid to a beneficiary.

Comparing SIPP Costs Sensibly

Headline rates rarely tell the full story. A sensible comparison looks at the total expected cost for a particular pot size, investment mix and trading pattern.

- Estimate platform fees on your expected pot value, including any caps.

- Estimate annual dealing fees based on how often you will trade.

- Add the OCFs of funds and trusts you intend to hold.

- Add any specialist fees for property, drawdown, in-specie transfers or annuity purchase.

- Stress-test by adjusting pot size up and down over 10 and 20 years.

- Consider service quality, FCA authorisation, scheme administrator reputation and FSCS coverage as well as price.

FSCS Cover for SIPPs

The Financial Services Compensation Scheme may pay compensation up to £85,000 per eligible person per FCA-regulated firm where the firm fails. Cover is broadly £85,000 per pension scheme member for investments. Cash deposits inside a SIPP held with a UK-regulated bank have a separate £85,000 limit per banking group, which rose to £120,000 from 1 December 2025 in some cases. FSCS does not protect against investment losses caused by market movements.

How Charges Affect Long-Term Outcomes

Even modest differences in annual charges compound dramatically over a working life. As a simple illustration only, an investor contributing the same amount each year and receiving the same gross return would end up with a meaningfully larger pension pot under a 0.4% total charge regime than under a 1.0% regime. These illustrations are highly sensitive to the assumed rate of return, contribution pattern and time horizon, but the direction of travel is consistent: lower ongoing costs typically support better long-term outcomes, all else equal.

Charges should therefore be reviewed regularly, not just at the point a SIPP is opened. As a pot grows, the most cost-effective fee structure can change — percentage-based platforms can become expensive at larger pot sizes, while flat-fee platforms can become cheaper. Many UK savers benefit from reviewing their pension charges every two to three years, particularly after material changes such as a Job move, a contribution increase or approaching the point of taking benefits.

Fees in Context

Charges are important but not the only Factor in choosing a SIPP. Wider investment menu, fund research, Customer Service, operator Due Diligence, the breadth of acceptable assets, online tools and the experience of opening, drawing or transferring the pension all matter. The cheapest provider is not always the right answer; the most expensive is not always premium.

Typical SIPP Fee Structures (Illustrative)

Illustrative ranges only. Always check current provider rate cards before deciding.

Key Takeaways

- SIPP fees include platform, dealing, fund and (where applicable) property charges.

- Percentage-based SIPPs suit smaller pots; flat-fee SIPPs can suit larger pots.

- Workplace default funds are capped at 0.75% per year; SIPPs are not.

- Full SIPPs that hold commercial property attract significant additional fees and require specialist advice.

- Always compare total expected cost, not headline rates, against your investment style and pot size.

- Service, FCA authorisation and FSCS cover should weigh alongside price.

- Regulated financial advice is recommended for transfers, consolidations and SIPP property decisions.

Please wait processing your request...

Please wait processing your request...