What Readers Need to Know

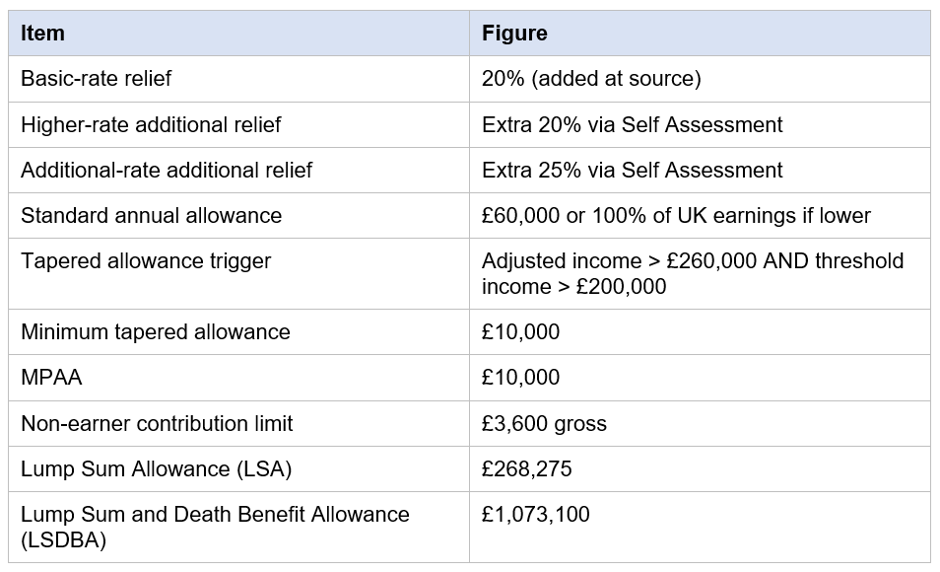

- SIPP contributions usually benefit from basic-rate tax relief at source — a contribution of £80 becomes £100 in the pension.

- Higher and additional-rate taxpayers can claim further tax relief through Self Assessment.

- The standard annual allowance for 2026/27 is £60,000 or 100% of UK Earnings if lower.

- Tapering reduces the annual allowance for high earners; the MPAA caps further DC contributions after flexible access.

- Specific tax outcomes depend on personal circumstances and a regulated adviser or Accountant should be consulted.

Introduction

Tax relief is the engine of UK pension saving. Without it, a SIPP would simply be another Investment account. With it, every contribution is topped up by the government — and for higher and additional-rate taxpayers, the boost can be substantial.

This guide explains how SIPP tax relief works in 2026/27, the allowances that cap it, how higher rates are claimed and the rules that can change the picture for high earners or anyone who has already started drawing a pension. It is general information for UK readers. Specific tax outcomes depend on personal circumstances and should be checked with a regulated adviser or accountant.

How SIPP Tax Relief Works at Source

Most SIPPs operate under a 'relief at source' model. The saver pays a contribution net of basic-rate tax — currently 20% — and the SIPP provider claims that 20% back from HMRC and credits it to the pension. In practice, an £80 contribution from Take-home pay becomes £100 inside the SIPP. The full £100 then benefits from gross compounding over time.

Relief at source is added automatically. There is nothing to claim for the basic-rate component, although it can take a few weeks for the Credit to arrive. The amount of relief is not affected by whether the saver actually paid basic-rate income tax in the year, but tax relief on personal contributions cannot exceed 100% of relevant UK earnings (or £3,600 gross for non-earners).

Higher and Additional Rate Relief

Relief through PAYE adjustment

HMRC can sometimes adjust the saver's tax code to deliver higher-rate relief through PAYE. This is less common for SIPP contributions, which are normally claimed via Self Assessment.

Employer Contributions to a SIPP

Some employers will pay contributions into a SIPP rather than a workplace pension, particularly for directors, contractors or senior employees. Employer contributions are usually paid gross and are typically allowable for corporation tax under the 'wholly and exclusively for the trade' test, but the rules on employer NICs, salary sacrifice and benefit-in-kind treatment can be complex. Tax advice is recommended.

The Annual Allowance

Money purchase annual allowance

Once a saver flexibly accesses a defined contribution pension — for example, by taking income from flexi-access drawdown or an uncrystallised funds pension lump sum — the £10,000 MPAA replaces the standard annual allowance for DC contributions. The MPAA is not subject to carry forward.

Carry Forward

Unused annual allowance from the previous three tax years can sometimes be carried forward to the current year, subject to having been a member of a registered pension scheme during those years. Carry forward does not apply to the MPAA. Carry forward calculations should be checked carefully — and ideally by a regulated adviser — before relying on them.

Tax-Free Cash and the LSA

Tax-free cash from a SIPP is capped under the Lump Sum Allowance (LSA) of £268,275, introduced from 6 April 2024 to replace the lifetime allowance regime. The Lump Sum and Death Benefit Allowance (LSDBA) of £1,073,100 sets the wider lifetime tax-free cap, including on death. Existing fixed and individual protections may preserve higher limits for some savers.

Other Tax Points UK Savers Should Note

- Income and gains generated inside a SIPP are generally free from UK income tax and Capital Gains Tax.

- Dividends received from UK shares inside a SIPP are not subject to UK Dividend tax.

- Dividend Withholding tax on overseas shares is not always reclaimable.

- Withdrawals from a SIPP above the LSA are taxed as income at the saver's marginal rate.

- Death benefits paid before age 75 are normally tax-free up to the LSDBA; after 75 they are taxed at the beneficiary's marginal rate.

Salary Sacrifice and SIPPs

Some employers operate salary sacrifice arrangements, where the employee gives up part of their salary in exchange for an employer pension contribution. The arrangement reduces both income tax and National Insurance for the employee and can reduce employer National Insurance as well. Salary sacrifice can support SIPP contributions where the employer agrees to pay into the saver's chosen SIPP. Tax outcomes depend on the arrangement and on whether minimum wage and benefit rules are affected; specialist advice is essential before changing salary structure.

Worked Examples (Illustrative Only)

Additional-rate taxpayer

An additional-rate taxpayer contributes £80 net. £20 is added at source. The saver can claim an additional £25 through Self Assessment, taking total effective relief to 45%.

Common SIPP Tax Relief Mistakes

Several mistakes appear regularly in HMRC and Financial Ombudsman Service cases involving SIPP contributions.

- Contributing more than 100% of relevant UK earnings, leading to refused relief.

- Forgetting to claim higher-rate relief through Self Assessment, leaving money on the table.

- Triggering the MPAA inadvertently by taking flexible drawdown, then contributing above £10,000.

- Misjudging the tapered annual allowance and exceeding the reduced limit.

- Failing to record gross contributions properly across multiple pensions.

Scottish Income Tax and SIPP Relief

Scottish taxpayers pay income tax at Scottish rates, which differ from rates and thresholds in the rest of the UK. SIPP providers still claim 20% relief at source for all UK savers under relief-at-source rules, but Scottish savers who pay tax at higher Scottish rates can claim additional relief through Self Assessment in the normal way. The exact amount of extra relief depends on the Scottish rate band applicable to each saver and should be checked with an adviser or accountant.

Net Pay Versus Relief at Source

Although most SIPPs use relief at source, workplace pensions sometimes use the 'net pay' arrangement instead. Under net pay, the contribution is deducted from gross pay before tax, so higher-rate taxpayers get full relief automatically without Self Assessment. Conversely, very low earners who would benefit from basic-rate relief at source may miss out under net pay if they earn below the personal allowance — although the government has introduced top-up arrangements to address this. SIPP savers should check which method applies to any workplace pension they also pay into, particularly when assessing total tax relief across all pensions.

When Tax Relief Can Be Lost or Clawed Back

- Annual allowance charge — applies where total contributions exceed the available annual allowance.

- MPAA charge — applies where DC contributions exceed £10,000 after flexible access.

- Tapered annual allowance charge — applies where high earners exceed their reduced allowance.

- Non-earner over-funding — relief is limited to £3,600 gross for non-earners.

- Contributions exceeding 100% of relevant UK earnings — excess relief can be denied or recovered.

Practical Tips Before Acting

- Check your earnings: tax relief on personal contributions cannot exceed 100% of relevant UK earnings.

- Check the annual allowance: include all pensions — workplace, personal and SIPP.

- Consider tapering: review threshold and adjusted income carefully if you earn near £200,000 or £260,000.

- Consider the MPAA: avoid triggering it inadvertently if you may want to keep contributing.

- Keep records: Self Assessment claims need supporting evidence of gross contributions.

- Speak to a regulated adviser or accountant before making large contributions or claims.

SIPP Tax Relief at a Glance (2026/27)

Key figures used in this article; verify against the HMRC Pensions Tax Manual at the time of any decision.

Key Takeaways

- SIPP contributions benefit from automatic basic-rate tax relief at source.

- Higher and additional-rate taxpayers should claim extra relief through Self Assessment.

- The annual allowance for 2026/27 is £60,000 — or 100% of UK earnings if lower.

- Tapering reduces the allowance for high earners; the MPAA caps DC contributions after flexible access.

- Carry forward of unused allowance can be powerful but requires careful calculation.

- Tax-free cash is capped by the LSA, with the LSDBA setting the wider lifetime tax-free cap.

- Regulated advice or accountancy input is recommended before large contributions or claims.

Please wait processing your request...

Please wait processing your request...