What Readers Need to Know

- SIPPs are FCA-regulated personal pensions but still carry Investment risk — values can fall as well as rise.

- More investment choice means more responsibility for the saver.

- Pension transfers, particularly from defined benefit schemes, carry significant risk and usually require advice.

- Pension scams have repeatedly used SIPP wrappers to hold unsuitable, Illiquid investments.

- Personal advice is recommended for transfers, consolidations and unusual investment choices.

Introduction

The Self-Invested Personal Pension has become a familiar feature of UK Retirement Planning, particularly for self-employed workers, contractors, higher earners and engaged investors. Its strengths are well documented — wide investment choice, tax relief and flexibility. Its risks deserve equal attention.

This article sets out the main risks UK savers should consider before opening a SIPP. It is general information for the 2026/27 tax year, not personal advice. A regulated financial adviser, free MoneyHelper guidance and Pension Wise appointments can help readers weigh the risks against their goals.

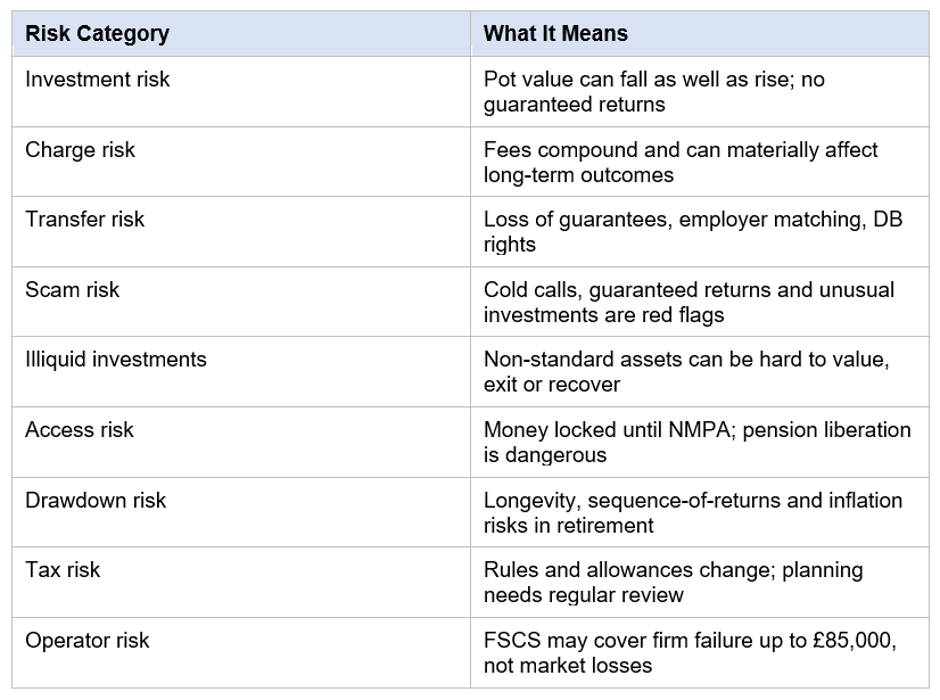

Investment Risk

All pension investments carry Market Risk. A SIPP holding shares, funds, ETFs or investment trusts will rise and fall with market values, and the saver bears the full risk of the choices made. Concentrated portfolios — single stocks, single sectors, single themes — can magnify both gains and losses. Even diversified portfolios are exposed to broad market downturns, currency movements and Interest Rate changes.

Past performance is not a guide to future returns. Long-term investment horizons reduce but do not eliminate the chance of losses.

Charge Risk

Fees compound over decades. A SIPP combining higher platform fees, frequent dealing and expensive funds can deliver materially worse outcomes than a low-cost alternative, even with identical underlying investments. Charges are not automatically a sign of quality.

- Platform fees can be percentage-based or flat, with very different break-even points.

- Dealing fees can erode returns where the saver trades frequently.

- Fund Ongoing Charges Figures (OCFs) range from under 0.10% for trackers to over 1% for some active strategies.

- Full SIPPs holding commercial property carry significant specialist fees on top of standard administration.

- Exit and transfer fees, though restricted by the FCA in many cases, can still apply.

Transfer Risk

Many SIPP openings involve transferring an existing pension — a workplace pension, an older personal pension or a defined benefit scheme — into the new SIPP. Transfers can mean losing valuable features and protections.

- Defined benefit (DB) transfers usually require regulated advice and have been a recurring concern for the FCA. The transfer value can be tempting but the loss of a guaranteed income for life is permanent.

- Workplace DC transfers can mean losing employer matching, guaranteed Annuity rates or scheme-specific benefits.

- Transfers triggered by aggressive cold calls or unsolicited contact are a classic feature of pension scams.

- Transfers of recent contributions can affect tax relief claims and trigger reporting.

Scam Risk

Pension scams have been a long-running focus for UK regulators. The FCA's ScamSmart campaign warns that 'guaranteed returns', 'unique investment opportunities' and 'free pension reviews' from cold callers are major red flags. SIPP wrappers have repeatedly been used to hold unsuitable or fraudulent investments — overseas property bonds, store pods, car park investments, forestry schemes and unregulated collective investment schemes (UCIS) — many of which have ended in losses for savers and FSCS compensation claims.

- Cold calls about pensions are banned in the UK — any cold call about a pension should be treated with extreme caution.

- Promised returns that are higher than mainstream investments are a red flag.

- High-pressure tactics — 'limited time offers', 'only if you decide today' — are warning signs.

- Advisers who are not on the FCA Register should not be trusted.

- Investments not on the SIPP operator's regular permitted list deserve extra Due Diligence.

Illiquid and Non-Standard Investments

SIPPs can hold non-standard investments where the SIPP operator allows them and the Assets meet HMRC rules. The FCA has tightened SIPP operator due diligence in recent years, but illiquid investments continue to cause problems: difficult valuations, slow exits, Capital write-offs and lengthy FOS or FSCS claims. UCIS, overseas property, micro-cap shares and structured products have all featured in past cases.

Access Risk

SIPP money is locked away until the normal minimum pension age — 55 in 2026, rising to 57 from 6 April 2028. Early access outside the rules can trigger pension liberation charges that can exceed 50% of the value. Schemes that promise to 'unlock' pensions before NMPA outside ill-health rules are almost always either non-compliant or fraudulent.

Drawdown and Longevity Risk

Once a saver starts drawing from a SIPP, two further risks come into play.

- Longevity risk — outliving the pension if withdrawals are too high relative to balance.

- Sequence-of-returns risk — withdrawing during market falls can permanently reduce sustainable income.

- Inflation risk — fixed withdrawals lose real value over time.

- MPAA — once Taxable Income is drawn, future DC contributions are capped at £10,000.

Tax Risk

Pension tax rules can change. The lifetime allowance was abolished from 6 April 2024 and replaced by the LSA (£268,275) and LSDBA (£1,073,100). Future legislation could change allowances, tapered allowance thresholds, the MPAA, the NMPA or the IHT treatment of pension death benefits. Plans built around current rules should be reviewed regularly.

Operator and Counterparty Risk

A SIPP relies on an FCA-regulated operator, an investment platform and the firms behind the underlying investments. Failures of any of these can disrupt the pension. The FSCS may pay compensation up to £85,000 per eligible person per firm where a claim is upheld, but cover does not protect against investment losses caused by market movements.

Behavioural Risks

Some of the biggest risks in a SIPP have nothing to do with markets or regulation. Engaged investors can be tempted into frequent trading, chasing themes or piling into recent winners. Each is easier in a SIPP — wide choice, online execution and self-direction make changes simple. Each can erode long-term returns. A written investment policy, an investment review schedule and adviser conversations all help keep behaviour in check.

Behavioural traps are not limited to active investors. Inattention is its own risk: failing to review contributions, charges or beneficiary nominations for years at a time can leave a SIPP misaligned with the saver's circumstances by the time benefits are taken.

Risk Outcomes Past Savers Have Faced

Public records from the Financial Ombudsman Service and the FSCS describe a range of poor outcomes UK SIPP savers have faced over the years.

- Transfers from valuable defined benefit pensions on the basis of misleading advice.

- SIPPs holding non-mainstream pooled investments that became worthless.

- Cold-calling 'introducer' firms steering savers into unsuitable SIPPs.

- High-pressure tactics to switch SIPP providers with no real benefit to the saver.

- Compounding of charges through frequent dealing or premium-priced funds without sufficient added value.

Building a More Resilient SIPP

These outcomes are not inevitable. Good due diligence, regulated advice and free guidance from MoneyHelper or Pension Wise can reduce the chance of falling into them. Resilient SIPP practice tends to share a few features: a written investment policy reviewed each year, a clear total-cost view including platform and fund OCFs, a diversified portfolio that does not depend on a single theme, and a willingness to ignore unsolicited offers however attractive they sound. None of these is exotic — they are simple disciplines that have stood the test of time.

Where to Get Help

UK savers can access free, impartial guidance through MoneyHelper (Money and Pensions Service). Pension Wise, provided through MoneyHelper, gives a free appointment to over-50s with DC pensions, including SIPPs. For personalised recommendations, the FCA Register lists regulated advisers. The Financial Ombudsman Service can help if a complaint cannot be resolved with the firm directly.

Key SIPP Risks at a Glance

A summary of the main risk categories for UK SIPP savers in 2026/27.

Key Takeaways

- SIPPs are powerful long-term wrappers, but more control means more responsibility.

- Investment risk, charges, transfers, scams and access rules are the key risk areas.

- Defined benefit transfers and unsolicited offers deserve particular caution.

- FSCS cover does not protect against market losses.

- Pension Wise (MoneyHelper) offers free guidance for over-50s with DC pensions.

- Regulated advice is recommended for transfers, consolidations and unusual investments.

- Regular review keeps plans aligned with changing rules and personal circumstances.

Please wait processing your request...

Please wait processing your request...